UNIT - 3

Cost and revenue are the two major factors that a profit maximizing firm needs to monitor continuously. It is the level of cost relative to revenue that determines the firm’s overall profitability. In order to maximize profits, a firm tries to increase its revenue and lower its cost. While the market factors determine the level of revenue to a great extent, the cost can be brought down either by producing the optimum level of output using the least cost combination of inputs, or increasing factor productivities, or by improving the organizational efficiency. The firm’s output level is determined by its cost.

Various Types of Costs:

There are different types of costs that a firm may consider relevant for decision-making under varying situations.

Direct and Indirect Costs

DIRECT COSTS

Direct costs are those costs which are incurred for producing a particular product and amount of expense is easily assignable to the product.

Example: The cost of the processor in a laptop manufacturing facility, producing two models X and Y, is a direct cost for the laptop. Why? It is explained by two things. One is the direct relation of the processor with the laptop. Every laptop uses one processor. Second is the traceability of the cost of the processor. Since one processor is used in a laptop, the cost of that processor can be completely assigned to the laptop. So, two checks are important for classifying any costs as a direct cost viz. relatedness and traceability.

INDIRECT COSTS

Indirect costs are those costs which are related to the product but are not traceable in an economically feasible manner.

Example: Salary of a supervisor of the laptop manufacturing utility for producing X and Y model. Why? It is simple. The supervisor supervises X model of laptop and Y too. But, it is very difficult to say that how much cost should be assigned to X and Y and finding out that may not be economically feasible. Here, we can see the relatedness is there since the manufacturing of X laptop requires the supervision of the supervisor but the traceability is not there as it is very difficult to trace how much supervision is on which model of laptop. The cause and effect relation between the product say Model X and the supervision cost is not direct and clear.

Direct costs are assigned to product based the relationship between the costs and the cost object whereas indirect costs are allocated based on some logical base.

For finding exact costing of a product, it is always desirable to have most part of costs as direct costs. But such a scenario is not practically possible. There are two main factors which affect the classification of costs into direct and indirect.

RECURRING COST

A cost that occurs repeatedly during the life of an asset, such as for periodic cleaning, guard service, or preventive maintenance. Such costs are most closely associated with facilities operations.

Non-recurring costs

Costs that occur on a one-time basis, and are unlikely to occur again in the normal course of business. Non-recurring costs include: capital expenditures, unusual charges, design, development and investment costs, various kinds of losses, legal costs, and moving expenses.

ariable Costs and Fixed Costs

All the costs faced by companies can be broken into two main categories: fixed costs and variable costs.

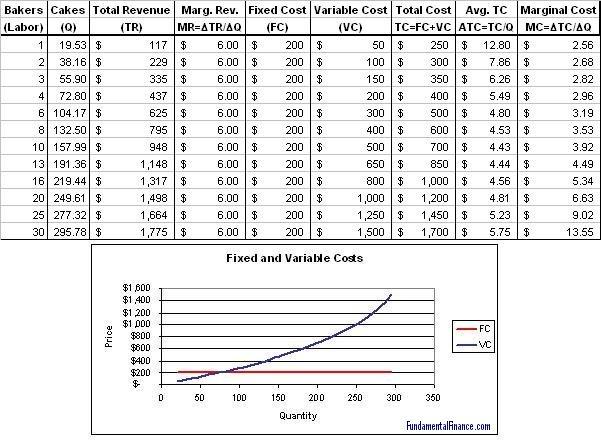

Fixed costs are costs that are independent of output. These remain constant throughout the relevant range and are usually considered sunk for the relevant range (not relevant to output decisions). Fixed costs often include rent, buildings, machinery, etc.

Variable costs are costs that vary with output. Generally variable costs increase at a constant rate relative to labor and capital. Variable costs may include wages, utilities, materials used in production, etc.

In accounting they also often refer to mixed costs. These are simply costs that are part fixed and part variable. An example could be electricity--electricity usage may increase with production but if nothing is produced a factory still may require a certain amount of power just to maintain itself.

Below is an example of a firm's cost schedule and a graph of the fixed and variable costs. Noticed that the fixed cost curve is flat and the variable cost curve has a constant upward slope.

SOURCES OF FINANCE

Business simply cannot function without money, and the money required to make a business function is known as business funds. Throughout the life of business, money is required continuously. Sources of funds are used in activities of the business. They are classified based on time period, ownership and control, and their source of generation.

Commercial Banks and Financial Institutions

Period Basis Sources

On the basis of the period, the different sources of funds can be classified into three parts. Which are:

Long-term sources fulfil the financial requirements of a business for a period more than 5 years. It includes various other sources such as shares and debentures, long-term borrowings and loans from financial institutions. Such financing is generally required for the procurement of fixed assets such as plant, equipment, machinery etc.

Medium-term sources are the sources where the funds are required for a period of more than one year but less than five years. The sources of the medium term include borrowings from commercial banks, public deposits, lease financing and loans from financial institutions.

Short-term sources: Funds which are required for a period not exceeding one year are called short-term sources. Trade credit, loans from commercial banks and commercial papers are the examples of the sources that provide funds for short duration.

Short-term financing is very common for the financing of present assets such as inventories and account receivables. Seasonal businesses that must build inventories in terms of future prospects of selling requirements often need short-term financing for the interim period between seasons. Wholesalers and manufacturers with a major portion of their assets used in inventories or receivables also require a large number of funds for a short period.

Ownership Basis Sources

On the basis of ownership, the sources can be classified into Owner’s funds and Borrowed funds. Owner’s funds mean funds which are procured by the owners of a business, which may be a sole entrepreneur or partners or shareholders of a business. It also includes profits which are reinvested in the business. The owner’s capital remains invested in the business for a longer duration and is not required to be refunded during the life period of the business.

This capital forms the base on which owners gain their right of control of management in the business. Some entrepreneurs may not like to dilute their ownership rights in the business and others may believe in sharing the risk. Equity shares and retained earnings are the two important sources from where owner’s funds can be obtained.

Borrowed funds refer to the funds raised with the help of loans or borrowings. This is the most common type of source of funds and is used the majority of the time. The sources for raising borrowed funds include loans from commercial banks, loans from financial institutions, issue of debentures, public deposits and trade credit.

These sources provide funds for a specific period, on certain terms and conditions and have to repay the loan after the expiry of that period with interest. A fixed rate of interest is paid by the borrowers on such loans. Often it does put a lot of burden on the business as payment of interest is to be made even when the earnings are low or when the loss is incurred. These institutions don’t take into consideration the activities of business after the loan is given. Generally, borrowed funds are provided on the security of some assets of the borrower.

Generation Basis Sources

The way of classifying the sources of funds is whether the funds are generated from within the organization or from external sources of the organization. Internal sources of funds are those that are generated inside the business. A business, for example, can generate funds internally by speeding collection of receivables, disposing of surplus inventories and increasing its profit. The internal sources of funds can fulfil only limited needs of the business.

Whereas, External sources of funds are the sources that lie outside an organization, such as suppliers, lenders, and investors. When a large amount of money is needed to be raised, it is generally done through the external sources. External funds may be costly as compared to those raised through internal sources.

In some cases, business is required to mortgage its assets as security while obtaining funds from external sources. The issue of debentures, borrowing from commercial banks and financial institutions and accepting public deposits are some of the examples of external sources of funds commonly used by business organizations.

Top-Down Budgeting

Top-down budgeting refers to a budgeting method where senior management prepares a high-level budget for the company. The company’s senior management prepares the budget based on its objectives and then passes it on to the managers for implementation.

Sometimes, the managers may put forward suggestions for the budget before the budget preparation, whether their contribution to the budgeting process will be used or not is at the management’s discretion. After the budget is created, the management makes specific allocations to the different departments, which must then create their own budgets based on their budget allocation and goals.

During top-down budgeting, the company’s management considers past experiences and current market conditions. They use the previous year’s budget and financial statements as a benchmark for making allocations to departments and functions. Senior management may take inputs from lower-level managers, which helps acknowledge the concerns of the regular staff who are tasked with implementing the budget. They also use internal and external influences such as prevailing economic conditions, changes in tax legislation, margin pressure, increase/decrease in salary costs, profitability levels of their peers, etc.

The Top-Down Budgeting Process

The top-down budgeting process starts with senior management meeting to come up with the objectives for the year. They discuss and determine high-level targets for the company in terms of sales, expenses, and profits. When formulating these figures, the management takes into account the contribution of each department in the previous year’s revenues. Usually, managers and lower level staff do not participate in the meetings but may put forward suggestions for consideration. Once the management finishes preparing the targets, the objectives are passed on to the finance department.

Budget Allocations to Departments

The finance department is tasked with making allocations to departments. The department may use the previous year’s figures to split the allocations. For example, if the marketing department incurred 10% of the overall expenses during the year, the finance department may allocate 10% of the total expenditure estimates for the next year.

The allocation may be higher or lower depending on what the departmental managers presented to the senior management. For example, if the company plans to roll-out a new product into the market, the finance department may increase the budget allocation for the marketing department to cover the promotional costs of the new product.

Department-level Budgets

Once the finance department assigns allocations to the various departments, department managers take the targets and prepare a budget of their own. Ideally, the work of the manager is to take the revenue and cost estimates and develop a budget that shows how the department will spend the allotted funds to generate the desired revenues.

Department-level budgets should include the specifics of expected expenditures, e.g., purchasing computers and office equipment, and salaries, as well as the projected number of products that the department aims to sell to generate revenues.

Harmonization of Departmental Budgets

Each department within the organization is then required to submit their budgets to the finance department for harmonization. The finance department reviews the department budgets to make sure they are aligned with the overall objectives of the company. If there are departments with insufficient or excess budgets, the finance department may send the budgets back for revision, and the allocations may be adjusted upwards or downwards.

Once the department budgets are completed and finalized, they are loaded onto the financial system to track monthly expenditures. Management deploys resources based on targets set by the budget. The departments receive monthly or periodic reports to show the amount of expenses incurred from the allocated budget, as well as the revenues generated vis-à-vis the department’s targets.

Advantages of Top-Down Budgeting

The budget features an overall corporate functional approach because senior management is concerned with the overall growth of the organization. It allows management to allocate resources to departments with a view to propelling the growth of the company, starting with the most critical department.

Top-down budgeting saves time for lower management. Rather than spending time creating a budget from scratch, lower-level managers are given an already-formulated budget to implement. It saves both time and resources that the managers would’ve had to use to formulate the budget.

Top-down budgeting creates one budget at a time, rather than allowing departments to develop their budgets and later combining them. As a result, the budgeting process will be less tedious, since senior management will formulate a single budget that the departments will follow. The departments are only allowed to create their budgets based on the targets set by the original budget from the top management. It makes the budget process quicker than bottom-up budgeting.

Disadvantages of Top-Down Budgeting

The level of motivation decreases since the managers who are required to implement the budget do not own the budget-making process. The managers do not take part in the preparation of the budget and may, therefore, lack incentive to ensure its success.

Senior managers are not involved in the day-to-day operations of the company, and they may not have realistic expectations of the expenses related to each department. Therefore, lower-level managers may find it difficult to implement the budget because they are unaware of how the top management arrived at the set targets. Also, the budget may be inaccurate since the targets for revenues and costs may be overstated or understated.

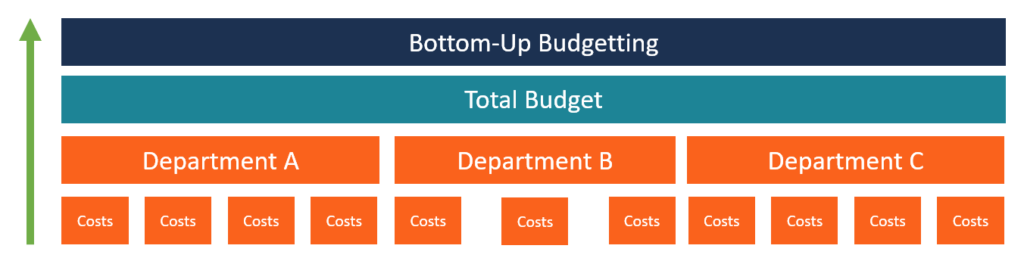

Bottom-Up Budgeting

Unlike top-down budgeting, bottom-up budgeting starts at the department level and moves up to the top management. The departmental heads/managers prepare their budget based on present information and past experiences and present it to the senior management for approval. They take into account margin pressures and market conditions to make the budget more realistic and attainable. The budget presented to top management contains an explanation of each item indicated in the budget.

BOTTOM-UP BUDGETING

Bottom-up budgeting is a budgeting method that starts at the department level to the top level. Each department within the organization is required to compile a list of the things it needs, the projects it plans to carry out in the next financial period, and the cost estimates. The estimates of all the departments are then summed up to get the overall company budget. The managers of each department are required to give their input since they know the cost estimates for the projects to be implemented.

How to Create a Bottom-up Budget

The following is the basic process that organizations follow when formulating a bottom-up budget:

1. Identify the individual components of the business

The first step when creating a bottom-up budget is to identify the individual components of the business and projects that the organization plans to carry out in the coming financial year. List the components and projects and establish the estimated cost to be incurred.

For example, a department may include costs like wages for employees, furniture and fittings, equipment purchases and hires, administrative costs, conference fees, etc. If the organization uses individual projects to get budget estimates, it must first obtain a list of all projects to be carried out in the coming year, and then come up with cost estimates for each project.

2. Get a sum of cost projections of each department

After each department finishes preparing a list of the planned projects and expenditures, the costs should be added up to get the total budget for each department. For example, the cost estimates of the human resource department may include $10,000 for recruiting personnel, $20,000 for employee salaries, and $6,000 for administrative costs, bringing the department’s total budget to $36,000. The departmental managers of other departments should come up with the totals of their respective departments.

3. Sum up the budgets of all departments

After getting the budgets of all the departments or identified projects, the budgets should be summed up to get the overall budget for the organization. The totals should be obtained from the departmental heads or head of projects appointed by the organization’s management.

4. Submit for approval

The final stage of the bottom-up budgeting process is submitting the budget estimates to the management for approval. When reviewing the budget, the management is interested in knowing if the budgets are aligned with the goals and objectives that the company wants to achieve in the next financial period.

If satisfied with the budget, the management will approve the budget estimates and send it to the finance department to make allocations to individual departments. However, if the company’s leadership is not satisfied with the budget estimates, they can ask the departmental managers to make the necessary changes before it can be submitted again for approval.

Advantages of Bottom-up Budgeting

The following are some of the benefits that organizations receive when they use bottom-up budgeting:

1. Better accuracy

Bottom-up budgeting calculates budget estimates from the lowest level, which helps boost the accuracy and accountability of the budget. The process involves all the individuals in each department. The estimates given will be as close as possible to reality since the employees are better placed to understand the costs, resources, expenses, and requirements of their respective departments and the entire organization. When the estimates for all departments are added up to get the overall budget, the senior management will know what to expect in the coming year.

2. Employee motivation

When employees are involved in the budget-making process, they will be motivated to work hard to achieve the organization’s goals. The employees in each department of the organization are involved in formulating the budget estimates, giving them a sense of ownership in the budget-making process.

Bottom-Up vs. Top-down Budgeting

Top-down budgeting and bottom-up budgeting are the two most popular types of budgets in corporate budgeting. Top-down budgeting starts with the senior management creating a budget for the entire organization and allocating budgets to the departments.

The departments are then required to create their own budget estimates that are confined to the amounts allocated by the top management. Although the top-down budgeting process takes less time, some departments may struggle to fit into the amounts allocated by management, since the management may not be aware of the goals that the departments plan to achieve.

On the other hand, bottom-up budgeting gives the departmental heads more power in contributing to the organizational budget. The department-level budget estimates are summed up to get the overall organizational budget that is sent to the senior management for approval.

The bottom-up budgeting process allows employees to own the process since they are familiar with the expenditures at the departmental levels. They will also be motivated to work hard since they feel that their input in the organization is valued by the management. On the downside, the departments may produce budgets that are off-target and not in-line with the company’s objectives. The budget will need to be modified to reflect the company objectives and remove unnecessary expenditures.

Activity Based Costing (ABC)

There are a number of costing models used in the domain of business and Activity-Based Costing is one of them. In activity-based costing, various activities in the organization are identified and assigned with a cost.

When it comes to pricing of products and services produced by the company, activity cost is calculated for activities that have been performed in the process of producing the products and services. In other words, activity-based costing assigns indirect costs to direct costs. These indirect costs are also known as overheads in the business world.

Let us take an example. There are a number of activities performed in a business organization and these activities belong to many departments and phases such as planning, manufacturing, or engineering. All these activities eventually contribute to producing products or offering services to the end clients.

Quality Control activity of a garment manufacturing company is one of the fine examples for such an activity. By identifying the cost for the Quality Control function, the management can recognize the costing for each product, service, or resource. This understanding helps the executive management to run the business organization smoothly.

Activity-based costing is more effective when used in long-term rather than in short-term.

Implementation in an Organization

When it comes to implementing activity-based costing in an organization, commitment of senior management is a must. Activity-based costing requires visionary leadership that should sustain long-term. Therefore, it is required that the senior management has comprehensive awareness of how activity-based costing works and management's interaction points with the process.

Before implementing activity-based costing for the entire organization, it is always a great idea to do a pilot run. The best candidate for this pilot run is the department that suffers from profit making deficiencies.

Although one might take it as risky, such departments may stand an opportunity to succeed when managed with activity-based costing. Lastly, this would give the organization a measurable illustration of activity-based costing and its success. In case, if no cost saving occurs after the pilot study is implemented, it is most likely that the model has not been properly implemented or the model does not suit the department or company as a whole.

Having a Core Team is Important

If an organization is planning to impalement activity-based costing, commissioning a core team is of great advantage. If the organization is small in scale, a team can be commissioned with the help of volunteers, who will contribute their time on part-time basis. This team is responsible for identifying and assessing the activities that should be revised in order to optimize the product or service.

The team should ideally consist of professionals from all practices in the organization. However, hiring an external consultant could also become a plus.

The Software

When implementing activity-based costing, it is advantageous for an organization to use computer software for calculations and data storage. The computer software can be a simple database that will store the information such as customized ABC software for the organization or a general-purpose off-the-shelf software.

The Procedure

The procedure for successful implementation of activity-based costing in an organization is as follows:

Identification of a team that is responsible for implementing activity-based costing.

The team identifies and assesses the activities that involve in products and services in question.

The team selects a subset of activities that should be taken for activity-based costing.

The team identifies the elements of selected activities that cost too much money for the organization. The team should pay attention to detail in this step as many activities may shield their cost and may look innocent from the outside.

The fixed costs and variable costs related to activities are identified.

The cost information gathered will be entered to the ABC software.

The software then performs calculations and produces reports to support management decisions.

Based on the reports, management can identify the steps that should be taken to increase profit margins in order to make the activities more efficient.

The management steps and decisions taken after an activity-based costing experience is generally known as Activity-Based Management. In this process, the management makes business decisions to optimize certain activities and let some activities go.

Things to be Aware of

Sometimes, organizations face the risk of spending too much time, money and resources on gathering and analysing data required for activity-based costing model. This can eventually lead to frustration and the organization may give up on ABC eventually.

Failure to connect the outcomes from the activity-based costing usually hinders the success of the implementation. This usually happens when the decision makers are not aware of the "big picture" of how activity-based costing can be used throughout the organization. Understanding the concepts and getting actively involved in the ABC implementation process can easily eliminate this.

If the business organization requires quick fixes, activity-based costing will not be the correct answer. Therefore, ABC should not be implemented for situations where quick wins are required.

Conclusion

Activity-based costing is a different way of looking at an organization's costs in order to optimize profit margins.

If ABC is implemented with the correct understanding for the correct purpose, it can return a great long-term value to the organization.

SOCIAL COST BENEFIT ANALYSIS (SCBA)

Rationale for SCBA

Market Imperfections.

Externalities.

Taxes and subsidies

Concern for savings.

Concern for Redistribution.

UNIDO Approach to SCBA

UNIDO approach emerged in 1960s. This approach was initially articulated in the “Guidelines for Project Evaluation” which provides a special framework for SCBA, especially in developed countries.

UNIDO method of project appraisal involves five stages

Calculation of the financial profitability of the project measured at market prices.

Obtaining the net benefit of the project measured in terms if economic (efficiency) prices.

Adjustment for the impact of the project on savings and investment.

Adjustment for the impact of the project on income and distribution.

Adjustment for the impact of the project on merit goods and demerit goods whose social values differ from their economic values.

Each of the above stages helps in feasibility of the project from different angles.

Stage 1- The measurement of financial profitability is similar to financial evaluation of the company.

Stage 2- It is concerned with determination of net benefits of the project in terms of economic (efficiency) prices. It is also called as shadow prices.

Stage 3 & 4- These stages are concerned with measuring the value of a project in terms of its contribution to savings and income redistribution. In order to make such assessment, the income gained or lost by individual groups in the society is measured.

Stage 5 – A merit good is one for which social value exceeds economic value. And a demerit good is one for which social value is less than economic value. The difference between social value and economic value has to be adjusted in the right direction.

Little-Mirrlees approach

I.M.D Little and J.A Mirrlees have developed an approach to social cost benefit analysiswhich became popular as Little-mirrlees approach (L-M approach).

There is a considerable similarity between the UNIDO approach and L-M approach.

Both approaches call for:

• Calculating accounting (shadow) prices particularly for foreign exchange savings and unskilled labour.

• Considering the factor of equity. • Use of DCF analysis.

Despite of the above similarities, there are some differences which are as follows:

• UNIDO approach is limited to domestic boundaries (measures cost and benefits in terms of domestic rupees) where as L-M approach considers international aspects also (measures cost and benefit in terms of international/border prices).

• UNIDO approach measures cost and benefits in terms of consumption where as the L-M approach measures cost and benefits in terms of uncommitted social income.

• The UNIDO approach focuses on efficiency, savings and redistribution aspects indifferent stages. L-M approach tends to view these aspects together.

No comments:

Post a Comment